Struggling with rising costs? Discover effective budgeting strategies to manage your finances better and reduce the stress caused by inflation.

Hey there, SimplVest fam. I’m a little upset…

I stopped by the supermarket yesterday to pick up a few things. Have you ever had one of those moments where you’re done shopping, look at your cart, then glance at the total and wonder how on earth things got so expensive? If there’s one thing I hate, it’s finding myself doing mental gymnastics and having to contemplate or even deciding what to put back on the shelf.

I realise I must not be alone with this. Right now, many of us are feeling the pinch, and it’s not just groceries—everything seems to be going up, from transportation to *gulp* rent. It’s enough to make anyone feel stressed about their finances.

The worst part is that there’s seemingly no way out—unless you plan to rob a bank (PLEASE, DON’T). We just have to buckle up and push forward. But here’s the thing: A little planning may go a long way in easing that stress. Building a budget might sound boring or restrictive, but it’s actually one of the most empowering things you can do for your financial health, especially right now.

And the best part? It doesn’t have to be complicated.

Let’s break it down with some straightforward budgeting strategies for building a better budget that works for you. They’re straightforward, easy to implement, and designed to help you stretch every naira, rand, or shilling a little further.

1. The Basics of Budgeting Strategies: Pen, Paper, or a Spreadsheet

Sometimes, simplicity is the key. Start by listing your income and expenses. You don’t need fancy tools—a piece of paper or a basic spreadsheet will do. On the left, write down all your income sources; on the right, jot down your fixed expenses like rent, utilities, and transportation. This old-school method helps you see exactly where your money is going, making it easier to adjust where needed.

Example: Let’s say you earn ₦200,000 monthly, and your fixed expenses are ₦150,000. This simple exercise will show you that you have ₦50,000 left for savings and other flexible spending, allowing you to prioritise better.

2. Go Digital: Try Budgeting Apps

For those who prefer tech solutions, budgeting apps can be a game-changer. Apps like Transfy, Cowrywise, Piggyvest, and Risevest link directly to your bank account and categorise your spending automatically. This gives you a clear picture of where your money is going and helps you stick to your budget without much manual effort.

Example: If you realise you’re spending too much on eating out, a budgeting app may be able to alert you, helping you cut back and redirect that money toward more essential expenses like savings or debt repayment.

3. Cash Stuffing: The Envelope Method

This is a popular method that’s making a comeback. The idea is simple: withdraw cash for your monthly expenses and divide it into envelopes labelled for specific categories like groceries, transportation, and entertainment. When an envelope is empty, you stop spending in that category.

Caution❗: While this method can be very effective in controlling spending, you’d do well to remember that keeping large amounts of cash at home can be risky. You might also miss out on the interest you could earn by keeping that money in a high-yield savings account.

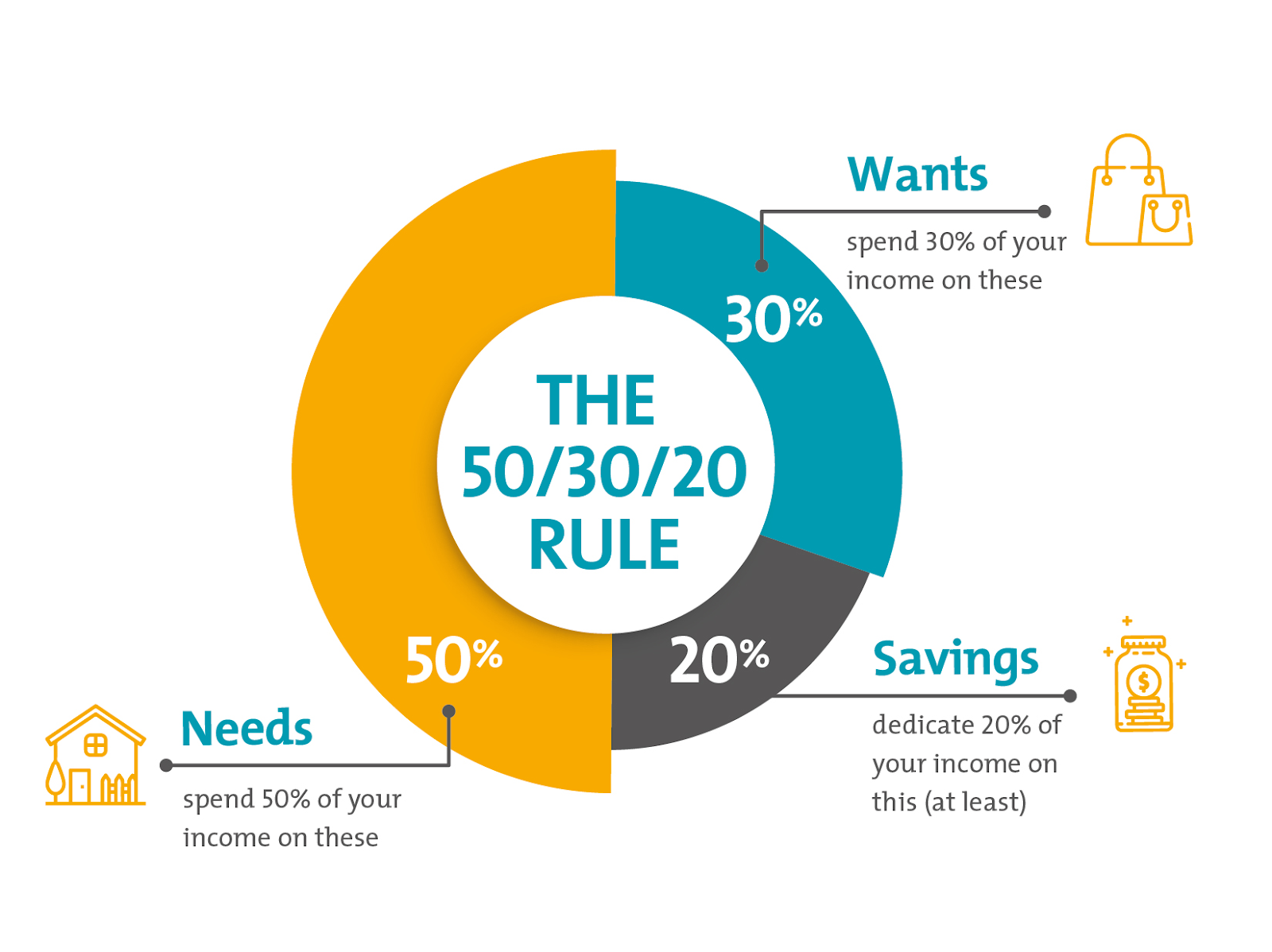

4. The 50/30/20 Rule: Prioritize Your Spending

This budgeting method suggests splitting your income into three categories: 50% for needs (rent, food, transportation), 30% for wants (dining out, entertainment), and 20% for savings. However, in high-cost cities like Lagos or Cape Town, you might need to adjust these percentages to fit your reality, possibly allocating more to needs and less to wants.

Example: If your monthly take-home pay is ₦250,000, you might allocate ₦150,000 (60%) to needs, ₦50,000 (20%) to wants, and ₦50,000 (20%) to savings. Adjust these percentages based on your situation, especially if you’re working towards a specific financial goal, like building an emergency fund.

5. Pay Yourself First with Reverse Budgeting

With reverse budgeting, the idea is to prioritise savings and investments before anything else. This method works well if you struggle with traditional budgeting strategies. Start by setting aside money for your goals—like retirement, emergency savings, or a down payment—then use the remainder for your needs and wants.

Example: If you save ₦40,000 first, and your total income is ₦200,000, you’ll have ₦160,000 left for everything else. This method ensures that you’re consistently building your savings without feeling deprived.

Look Out for Common Budgeting Pitfalls: Plan for Big Expenses

Housing, transportation, and food take up the largest portions of most people’s budgets. Focus on controlling costs in these areas to make the biggest impact. Also, don’t forget to plan for irregular expenses like car repairs or school fees. A “sinking fund”—setting aside a little each month—can help you manage these costs without derailing your budget.

Tip: If you’re sharing expenses with a partner or roommate, communicate regularly to keep everyone on the same page. The key thing to remember about budgeting is that you don’t have to be perfect; instead, it’s all about how you make steady progress.

Final Thoughts

Budgeting strategies during times of high inflation can feel challenging, but with a little planning and the right strategies, you can stay on top of your finances. And it’s no big deal; no one will grade your budget— so do your best and adjust as needed. And if one method doesn’t work for you, don’t hesitate to try another until you find the right fit.

Want more tips on managing your money and making smart financial moves? Check out our clusters on related topics.

Until next time,

Dami from SimplVest 🚀